Atten Babler Corn & Soybeans FX Indices – Mar…

Corn FX Indices:

The Atten Babler Commodities Corn Foreign Exchange (FX) Indices weakened throughout Feb ’22. The USD/Corn Exporter FX Index and USD/Corn Importer FX Index each declined to three month low levels while the USD/Domestic Corn Importer FX Index declined to a four month low level throughout the previous month.

Global Corn Net Trade:

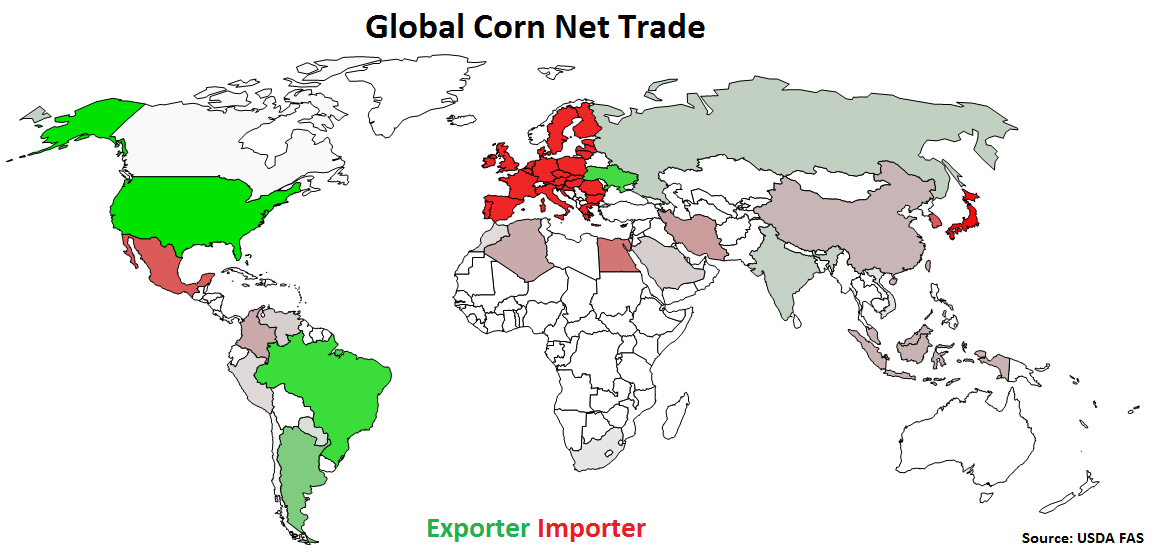

Major net corn exporters are led by the U.S., followed by Brazil, Ukraine, Argentina, Russia and India (represented in green in the chart below). Major net corn importers are led by the EU-28, followed by Japan, Mexico, South Korea, Egypt and Iran (represented in red in the chart below).

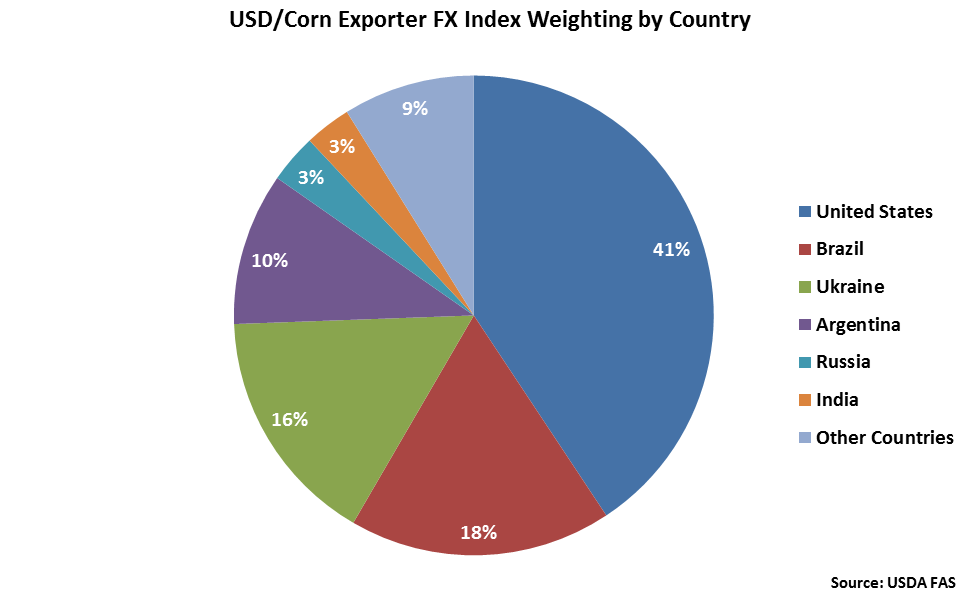

The United States accounts for over two fifths of the USD/Corn Exporter FX Index, followed by Brazil at 18%, Ukraine at 16% and Argentina at 10%.

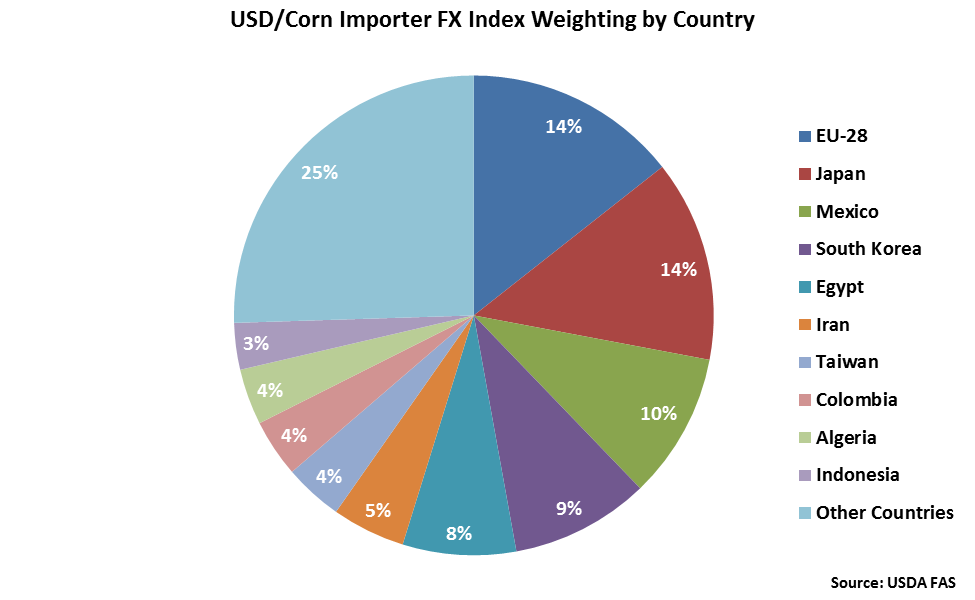

The EU-28 and Japan each account for 14% of the USD/Corn Importer FX Index. Mexico, South Korea, Egypt and Iran each account for between 5-10% of the index.

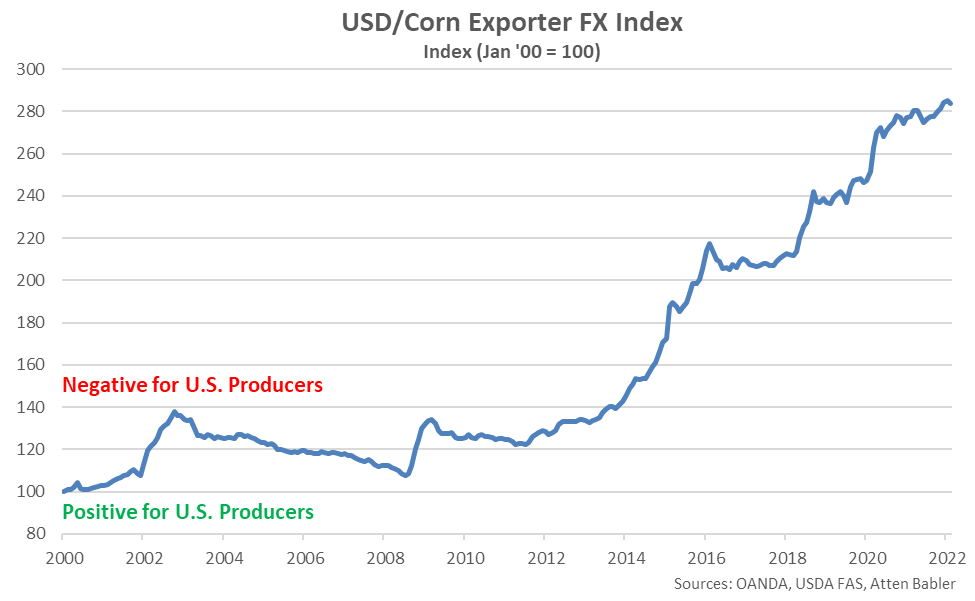

USD/Corn Exporter FX Index:

The USD/Corn Exporter FX Index declined 1.2 points throughout Feb ’22, finishing at a three month low value of 283.9. The USD/Corn Exporter FX Index remained up 6.3 points throughout the past six months and 141.4 points since the beginning of 2014, despite the most recent decline. A strong USD/Corn Exporter FX Index reduces the competitiveness of U.S. corn relative to other exporting regions (represented in green in the Global Corn Net Trade chart), ultimately resulting in less foreign demand, all other factors being equal. USD appreciation against the Argentine peso and Ukrainian hryvnia has accounted for the majority of the gains since the beginning of 2014.

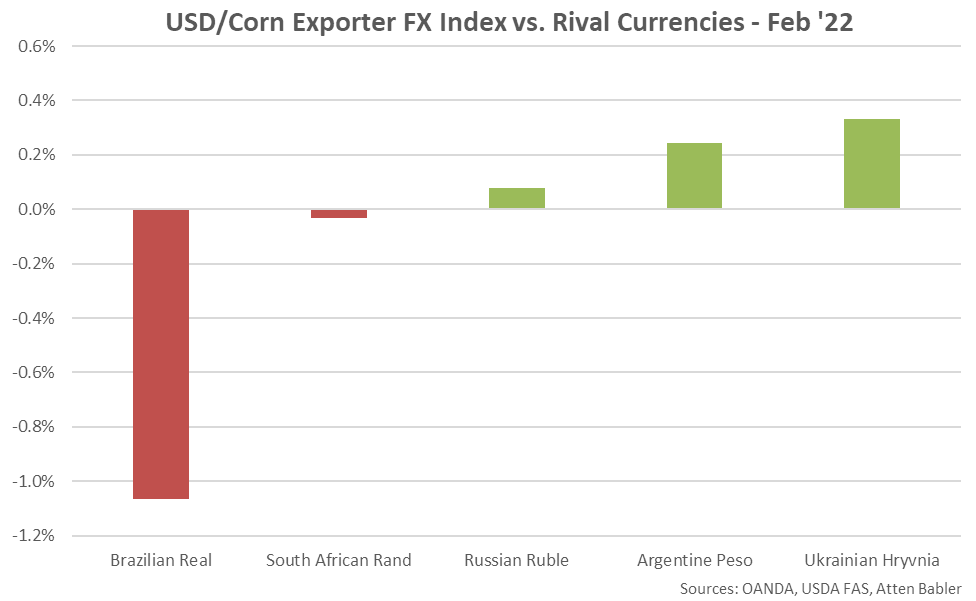

Appreciation against the USD within the USD/Corn Exporter FX Index during Feb ’22 was led by gains by the Brazilian real, followed by gains by the South African rand. USD gains were experienced against the Ukrainian hryvnia, Argentine peso and Russian ruble.

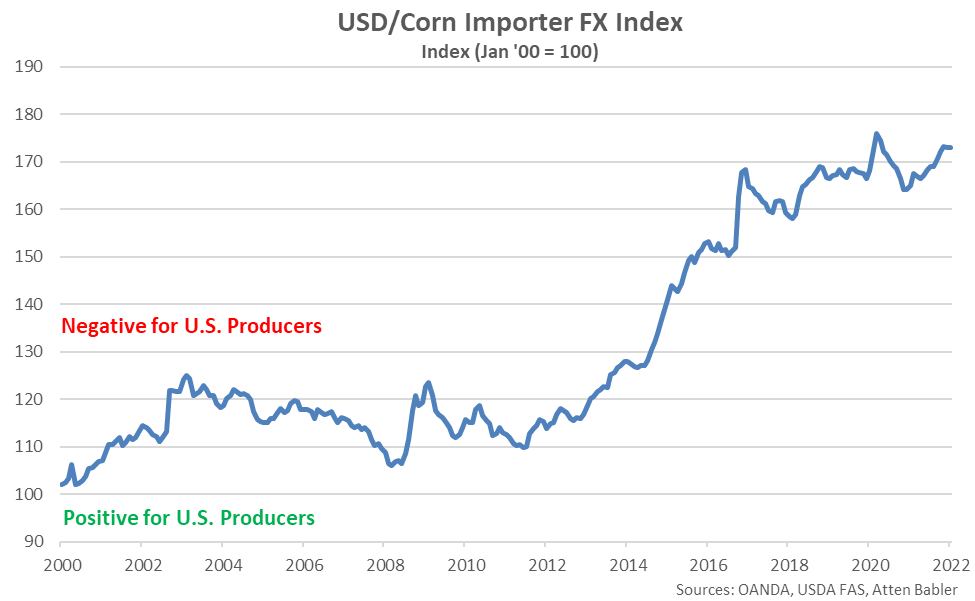

USD/Corn Importer FX Index:

The USD/Corn Importer FX Index declined 0.1 point throughout Feb ’22, finishing at a three month low value of 173.1. The USD/Corn Importer FX Index remained up 4.1 points throughout the past six months and 46.1 points since the beginning of 2014, despite the most recent decline. A strong USD/Corn Importer FX Index results in less purchasing power for major corn importing countries (represented in red in the Global Corn Net Trade chart), making U.S. corn more expensive to import. USD appreciation against the Egyptian pound, Mexican peso, euro and Iranian rial has accounted for the majority of the gains since the beginning of 2014.

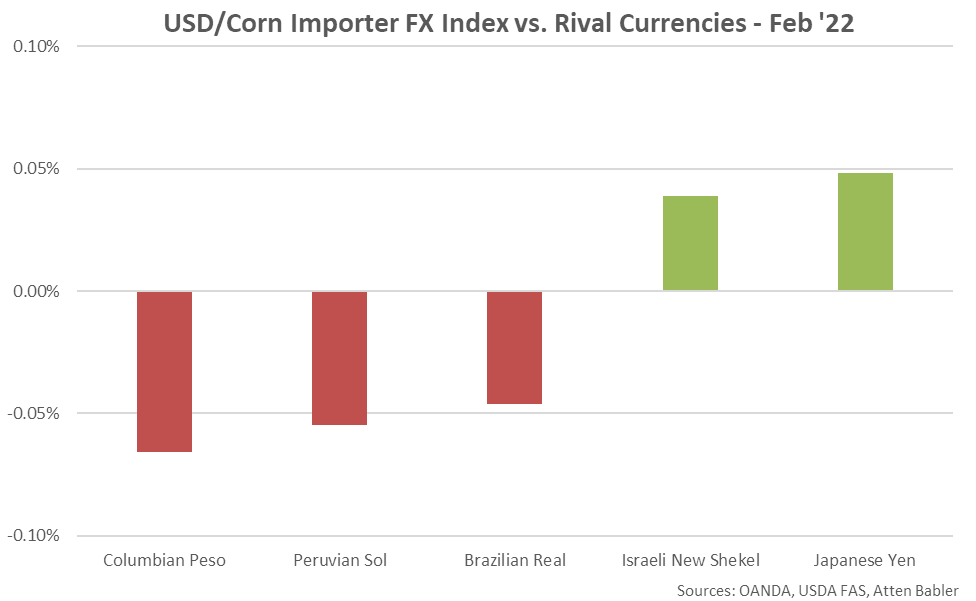

Appreciation against the USD within the USD/Corn Importer FX Index during Feb ’22 was led by gains by the Columbian peso, followed by gains by the Peruvian sol and Brazilian real. USD gains were experienced against the Japanese yen and Israeli new shekel.

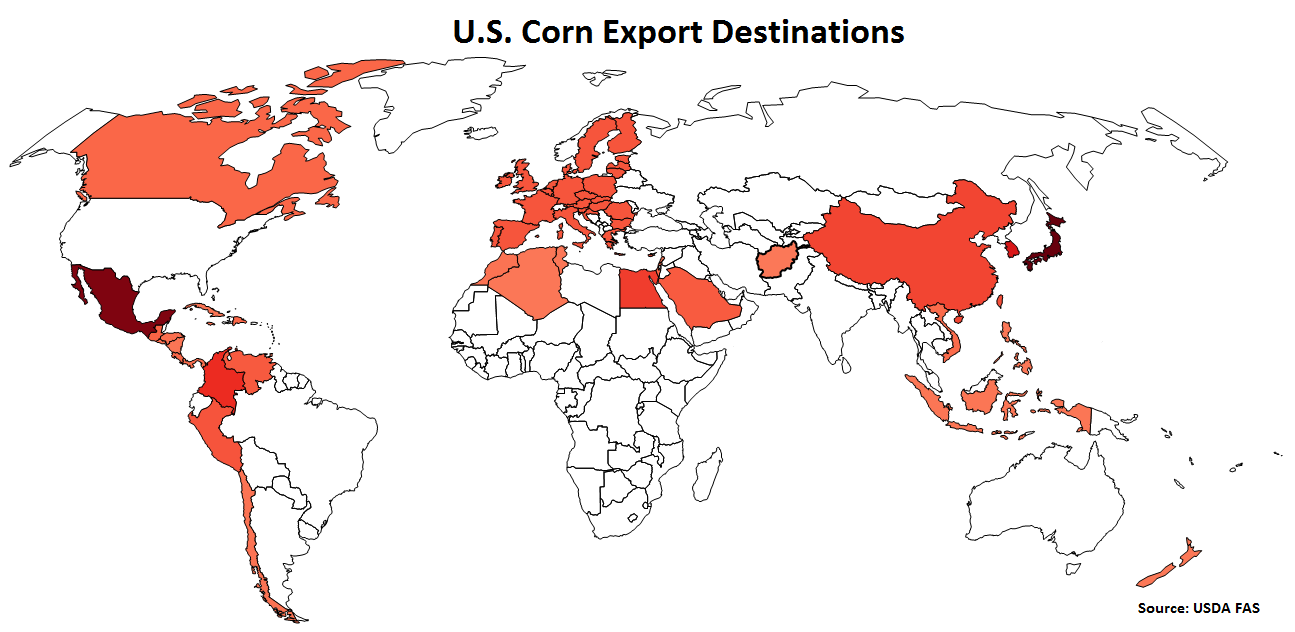

U.S. Corn Export Destinations:

Major destinations for U.S. corn are led by Japan, followed by Mexico, South Korea, Columbia, Egypt and China.

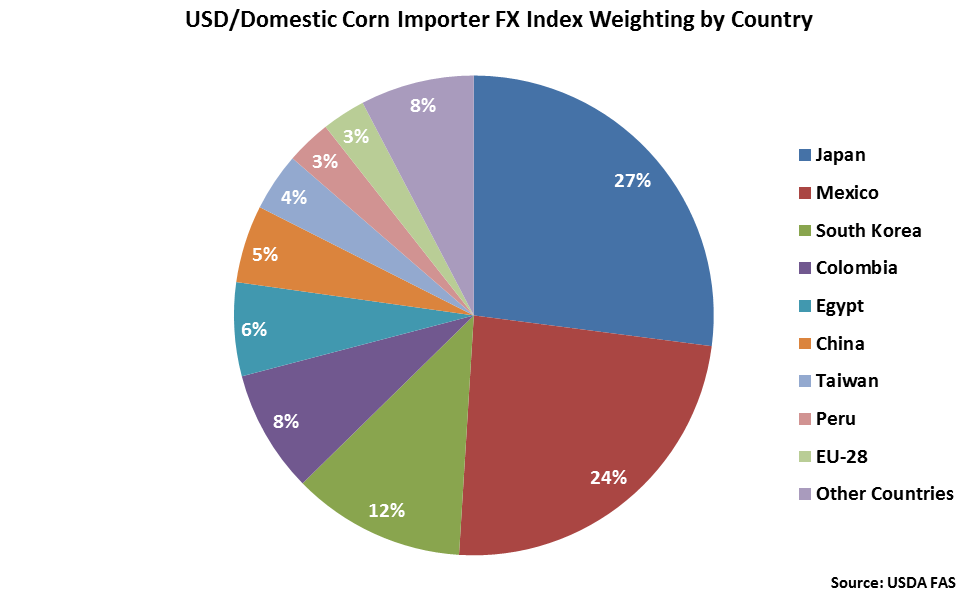

Japan accounts for 27% of the USD/Domestic Corn Importer FX Index, followed by Mexico at 24% and South Korea at 12%. Columbia, Egypt and China each account for between 5-10% of the index.

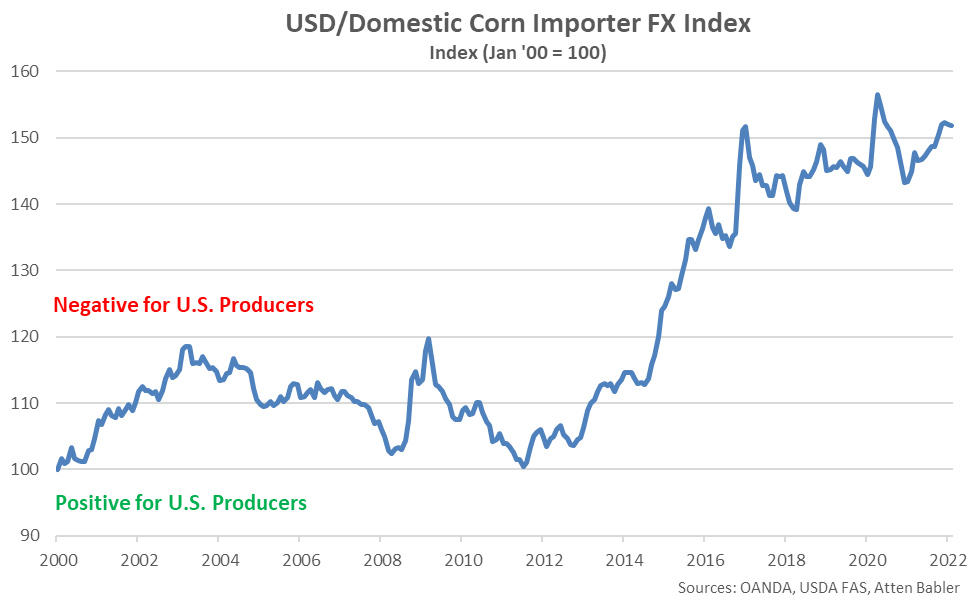

USD/Domestic Corn Importer FX Index:

The USD/Domestic Corn Importer FX Index declined 0.2 points throughout Feb ’22, finishing at a four month low value of 151.8. The USD/Domestic Corn Importer FX Index remained up 3.1 points throughout the past six months and 38.2 points since the beginning of 2014, despite the most recent decline. A strong USD/Domestic Corn Importer FX Index results in less purchasing power for the traditional buyers of U.S. corn (represented in red in the U.S. Corn Export Destinations chart), ultimately resulting in less foreign demand, all other factors being equal. USD appreciation against the Mexican peso and has accounted for the majority of the gains since the beginning of 2014.

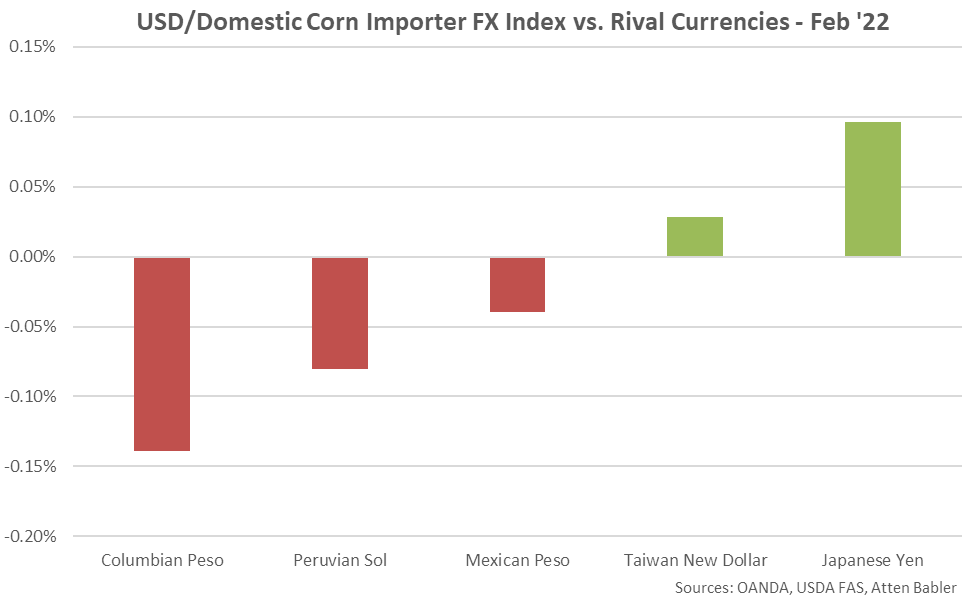

Appreciation against the USD within the USD/Domestic Corn Importer FX Index during Feb ’22 was led by gains by the Columbian peso, followed by gains by the Peruvian sol and Mexican peso. USD gains were experienced against the Japanese yen and Taiwan new dollar.

Soybeans FX Indices:

The Atten Babler Commodities Soybeans Foreign Exchange (FX) Indices weakened throughout Feb ’22. The USD/Soybean Exporter FX Index and USD/Domestic Soybean Importer FX Index each declined to five month low levels while the USD/Soybean Importer FX Index declined to a three month low level throughout the previous month.

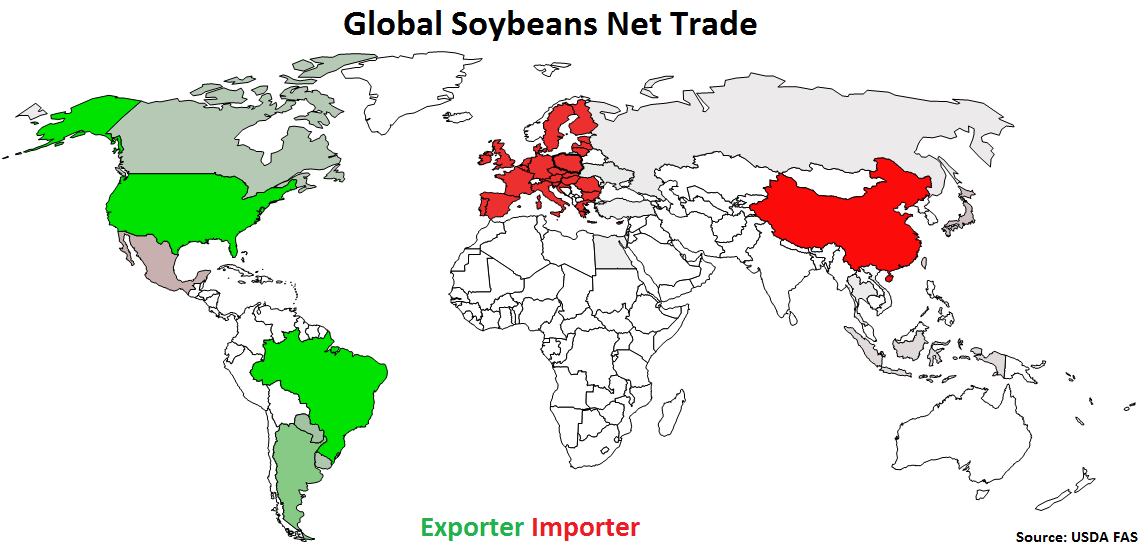

Global Soybeans Net Trade:

Major net soybeans exporters are led by Brazil, followed by the U.S., Argentina, Paraguay and Canada (represented in green in the chart below). Major net soybeans importers are led by China, followed by the EU-28, Mexico and Japan (represented in red in the chart below).

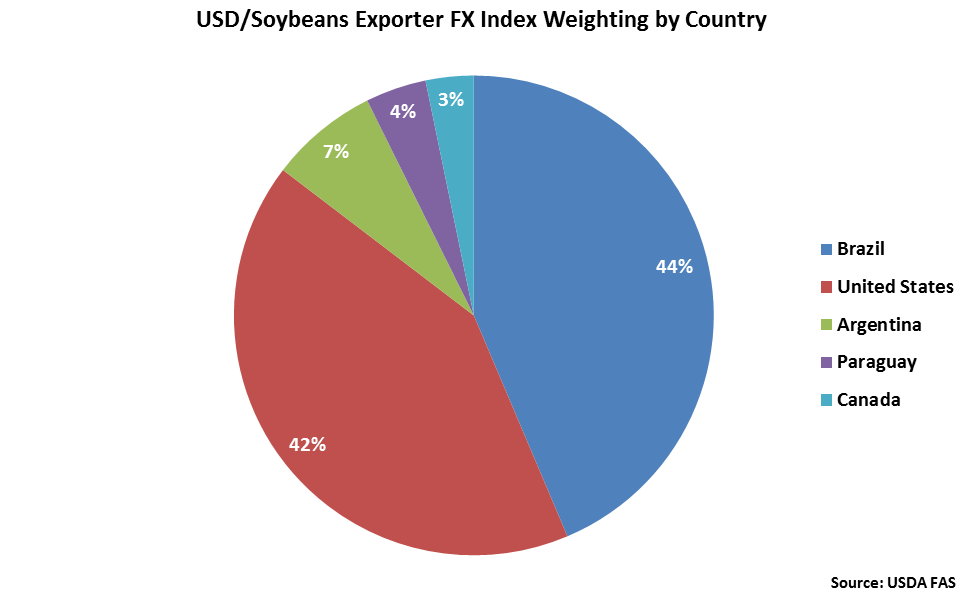

Brazil and the United States each account for over two fifths of the USD/Soybeans Exporter FX Index, followed by Argentina at 7%.

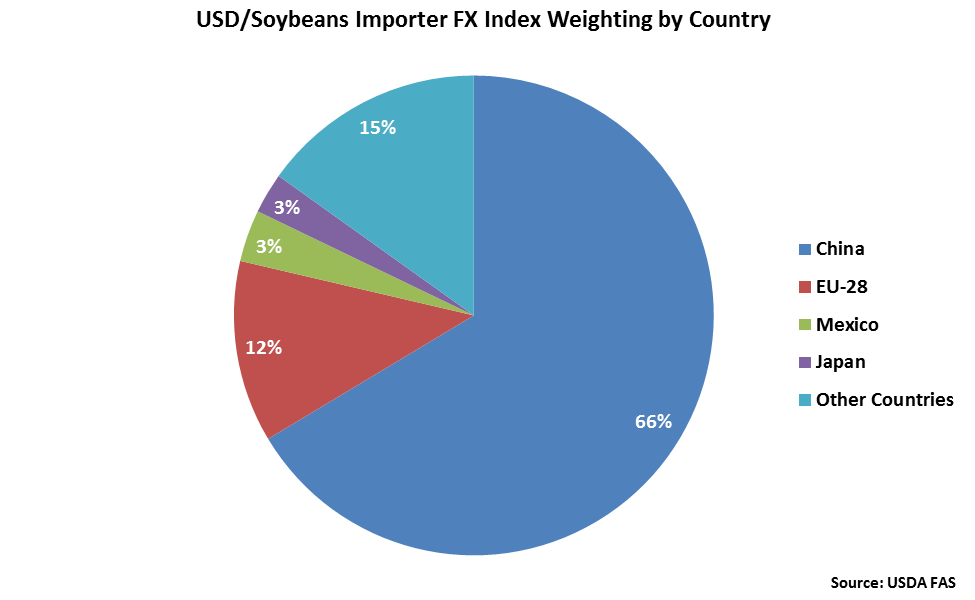

China accounts for nearly two thirds of the USD/Soybeans Importer FX Index, followed by the EU-28 at 12%.

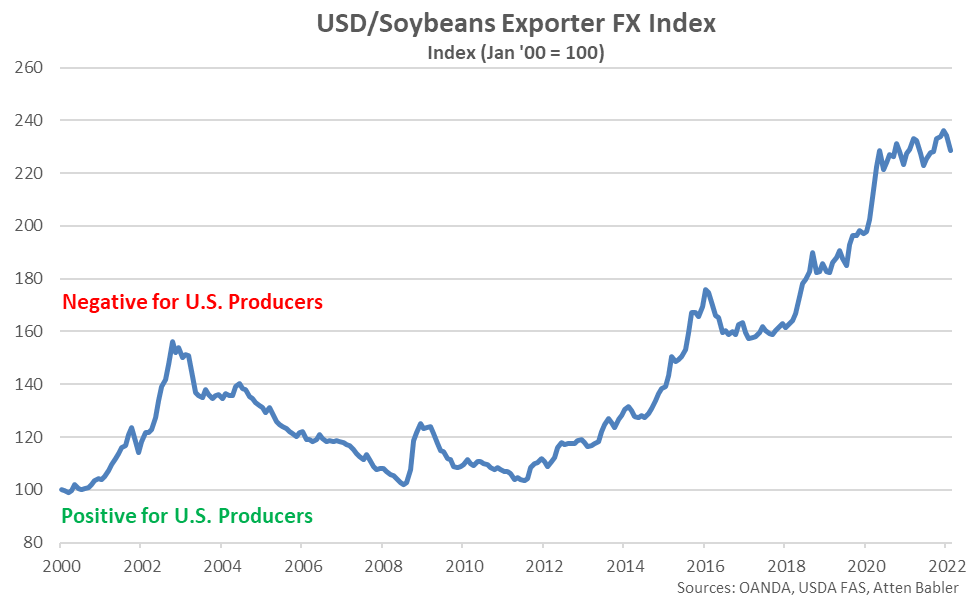

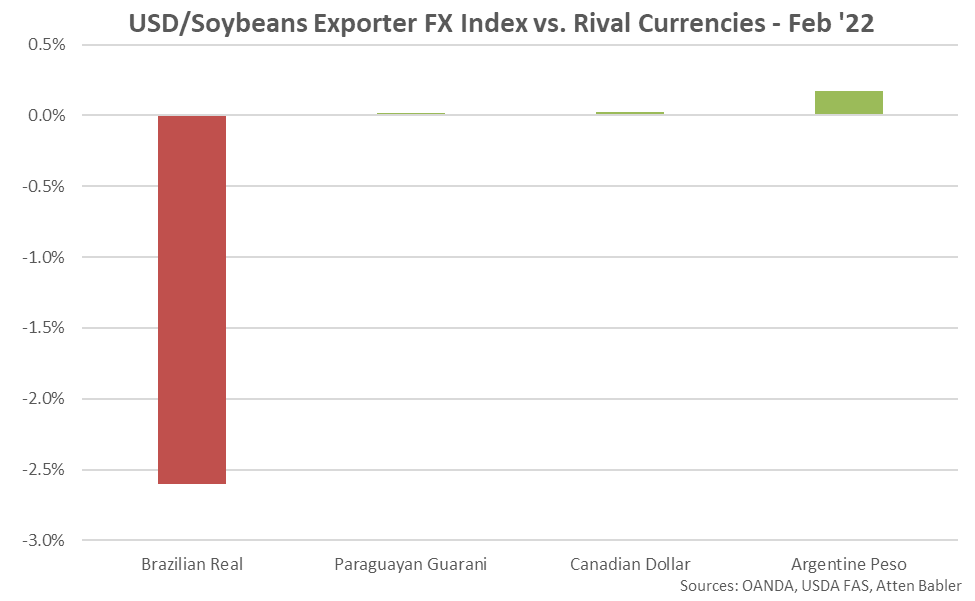

USD/Soybeans Exporter FX Index:

The USD/Soybeans Exporter FX Index declined 5.6 points throughout Feb ’22, finishing at a five month low value of 228.4. USD/Soybeans Exporter FX Index remained up 0.7 points throughout the past six months and 100.1 points since the beginning of 2014, despite the most recent decline. A strong USD/Soybeans Exporter FX Index reduces the competitiveness of U.S. soybeans relative to other exporting regions (represented in green in the Global Soybeans Net Trade chart), ultimately resulting in less foreign demand, all other factors being equal. USD appreciation against the Brazilian real has accounted for the majority of the gains since the beginning of 2014.

Appreciation against the USD within the USD/Soybeans Exporter FX Index during Feb ’22 was led by gains by the Brazilian real. USD gains were experienced against the Argentine peso, Canadian dollar and Paraguayan guarani.

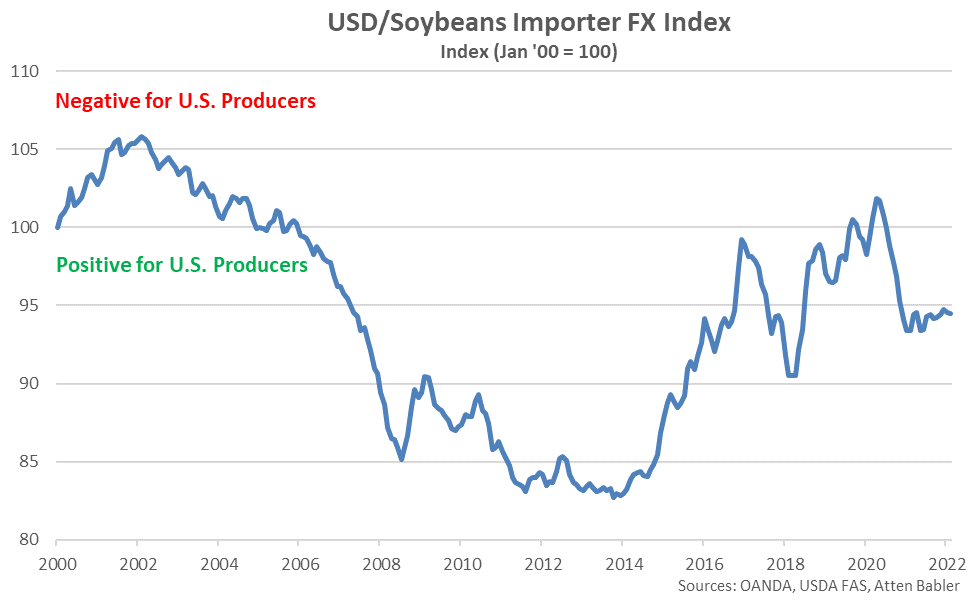

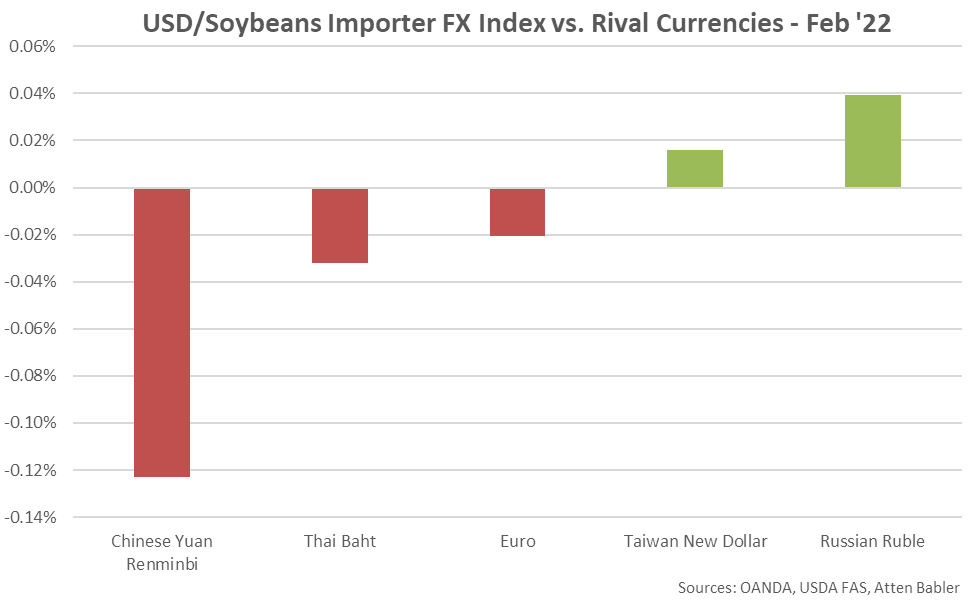

USD/Soybeans Importer FX Index:

The USD/Soybeans Importer FX Index declined 0.1 point during Feb ’22, finishing at a three month low value of 94.5. The USD/Soybeans Importer FX Index remained up 0.1 point throughout the past six months and 11.6 points since the beginning of 2014, despite the most recent decline. A strong USD/Soybeans Importer FX Index results in less purchasing power for major soybeans importing countries (represented in red in the Global Soybeans Net Trade chart), making U.S. soybeans more expensive to import. USD appreciation against the Chinese yuan renminbi has accounted for the majority of the gains since the beginning of 2014.

Appreciation against the USD within the USD/Soybeans Importer FX Index during Feb ’22 was led by gains by the Chinese yuan renminbi, followed by gains by the Thai baht and euro. USD gains were experienced against the Russian ruble and Taiwan new dollar.

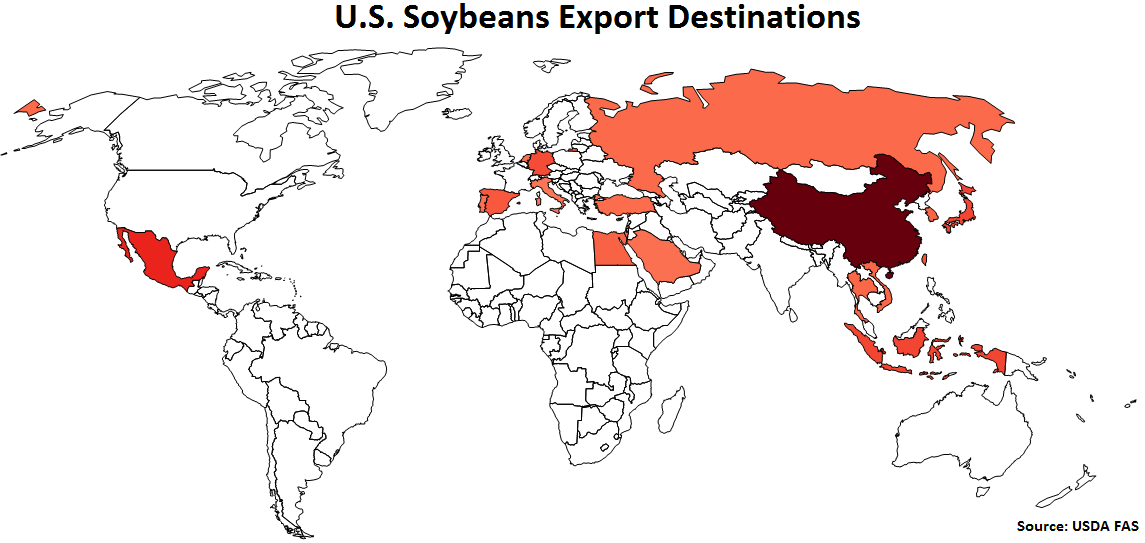

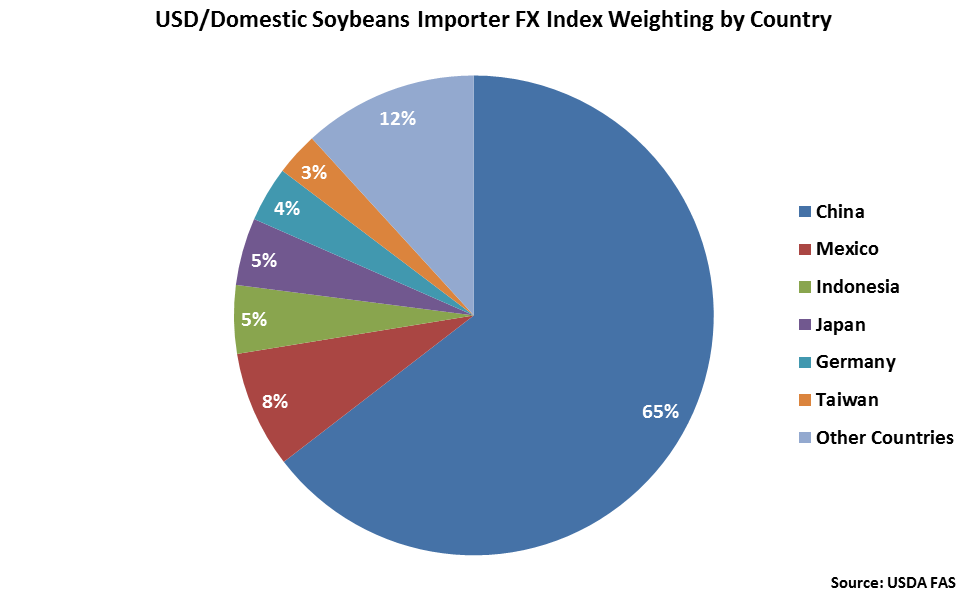

U.S. Soybeans Export Destinations:

Major destinations for U.S. soybeans are led by China, followed by Mexico, Indonesia and Japan.

China accounts for nearly two thirds of the USD/Domestic Soybeans Importer FX Index. Mexico, Indonesia and Japan each account for between 5-10% of the index.

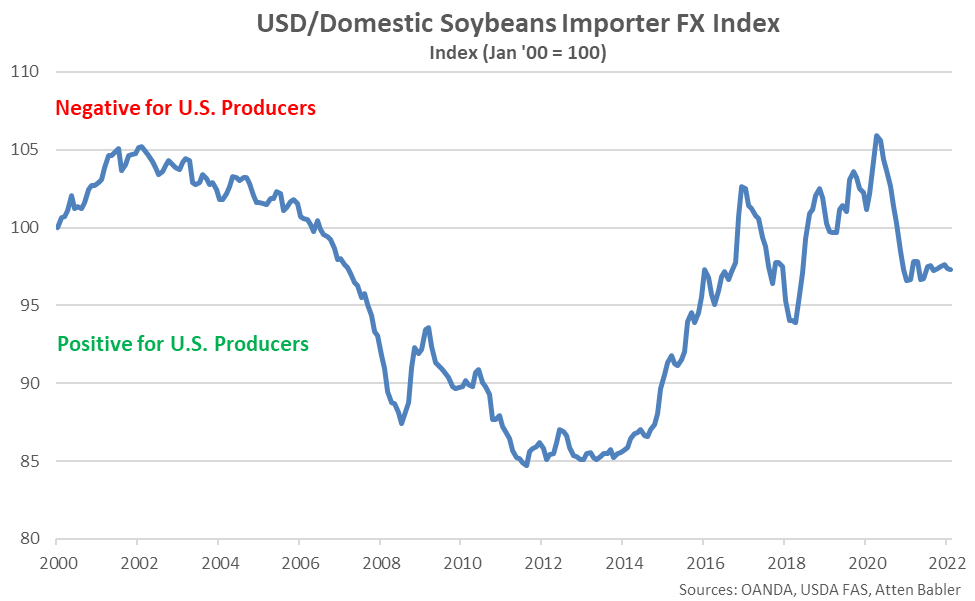

USD/Domestic Soybeans Importer FX Index:

The USD/Domestic Soybeans Importer FX Index declined 0.1 point throughout Feb ’22, finishing at a five month low value of 97.3. The USD/Domestic Soybeans Importer FX Index has declined 0.2 points throughout the past six months but has remained up 11.8 points since the beginning of 2014, despite the most recent decline. A strong USD/Domestic Soybeans Importer FX Index results in less purchasing power for the traditional buyers of U.S. soybeans (represented in red in the U.S. Soybeans Export Destinations chart), ultimately resulting in less foreign demand, all other factors being equal. USD appreciation against the Chinese yuan renminbi has accounted for the majority of the gains since the beginning of 2014.

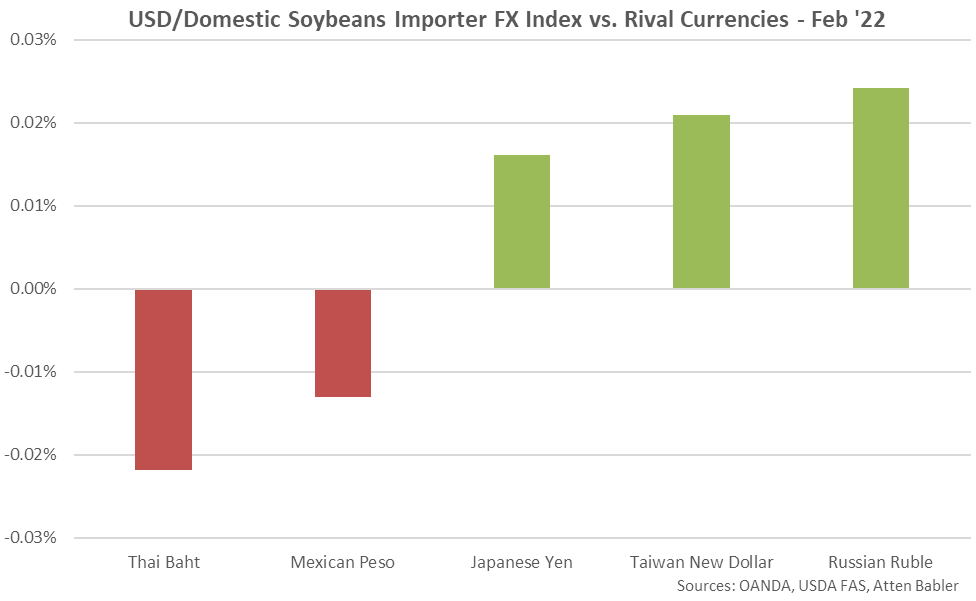

Appreciation against the USD within the USD/Domestic Soybeans Importer FX Index during Feb ’22 was led by gains by the Thai baht, followed by gains by the Mexican peso. USD gains were experienced against the Russian ruble, Taiwan new dollar and Japanese yen.