U.S. Livestock & Meat Trade Update – Mar ’16

Executive Summary

U.S. livestock and meat trade figures provided by USDA were recently updated with values spanning through Jan ’16. Highlights from the updated report include:

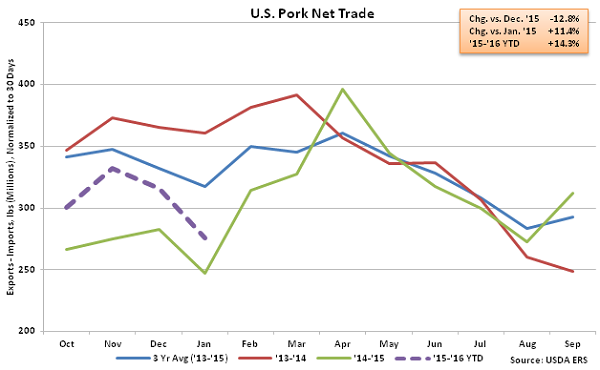

• Net pork trade remained higher on a YOY basis for the sixth consecutive month, finishing 11.4% above the previous year as export volumes remained strong.

• Net beef trade declined to a four month low as import volumes increased sharply, finishing 54.1% higher than the previous year.

• Broiler exports declined on a YOY basis for the 15th time in the past 16 months, finishing down 6.8% to a five year low for the month of January.

Additional Report Details

Pork – YOY Net Trade Remains Higher on Strong Exports

According to USDA, Jan ’16 U.S. pork export volumes declined 10.6% MOM on a daily average basis but remained higher on a YOY basis for the sixth consecutive month, increasing by 10.1%. Of the major export destinations, YOY gains in export volumes were led by combined shipments to Hong Kong, Taiwan and China (+189.3%), followed by shipments to Japan (+9.4%). The YOY gains in shipments to China and Japan more than offset declines in U.S. pork exports to South Korea (-16.0%), Canada (-4.7%) and Mexico (-3.4%). U.S. pork exports to the aforementioned countries accounted for nearly 85% of all pork export volumes during Jan ’16.

Jan ’16 U.S. pork imports finished higher on a YOY basis for the 19th time in the past 23 months, increasing 6.6% to a record high for the month of January. Jan ’16 U.S. net pork trade finished up 11.4% YOY as increases in export volumes continue to outweigh strong import volumes. ’14-’15 annual net pork trade finished down 10.0% to a new five year low, however ’15-’16 net pork trade is up 14.3% YOY throughout the first third of the production season.

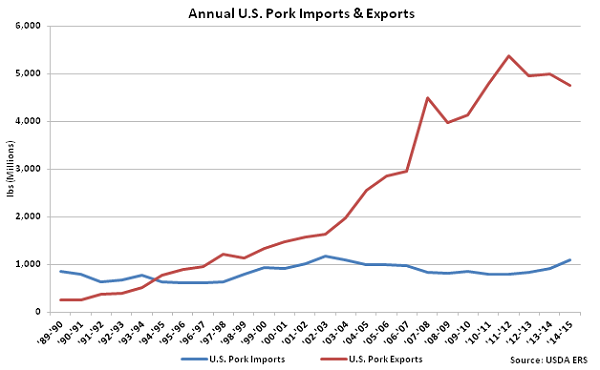

U.S. pork export volumes have strengthened considerably over the past 25 years, increasing at a compound annual growth rate (CAGR) of 13.2%, while U.S. pork imports have remained fairly flat, increasing at a CAGR of 0.3% over the same time period. ’13-’14 annual pork imports experienced much stronger growth, finishing 10.5% higher than the previous year, the largest YOY percentage gain in 11 years. Despite the increase in pork imports, ’13-’14 annual pork exports volumes remained over five times as large as import volumes. Pork export volumes remained over four times as large as import volumes throughout the ’14-’15 production season despite declining to a five year low on an absolute basis.

U.S. pork export volumes have strengthened considerably over the past 25 years, increasing at a compound annual growth rate (CAGR) of 13.2%, while U.S. pork imports have remained fairly flat, increasing at a CAGR of 0.3% over the same time period. ’13-’14 annual pork imports experienced much stronger growth, finishing 10.5% higher than the previous year, the largest YOY percentage gain in 11 years. Despite the increase in pork imports, ’13-’14 annual pork exports volumes remained over five times as large as import volumes. Pork export volumes remained over four times as large as import volumes throughout the ’14-’15 production season despite declining to a five year low on an absolute basis.

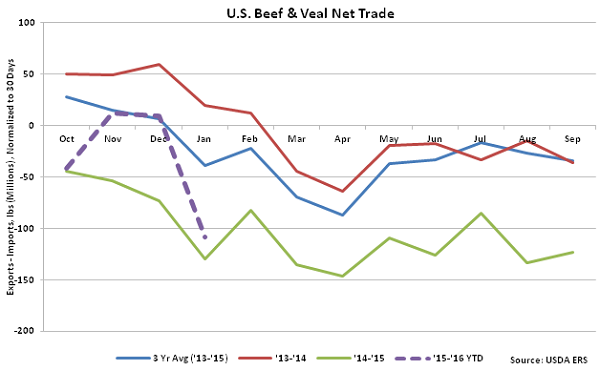

Beef & Veal – Net Trade Declines to Four Month Low on Strong Imports

Jan ’16 U.S. beef & veal export volumes declined 10.9% MOM on a daily average basis but increased on a YOY basis for the first time in 16 months, finishing 7.4% above the previous year’s levels. Of the major export destinations, YOY increases in export volumes were led by South Korea (+51.7%), followed by Japan (+18.4%) and combined volumes to Hong Kong, Taiwan and China (+17.5%). The YOY gains in shipments to South Korea, Japan and China more than offset declines in U.S. beef & veal exports to Mexico (-27.0%) and Canada (-8.0%). U.S. beef & veal exports to the aforementioned countries accounted for over 85% of all beef & veal export volumes during Jan ’16.

Jan ’16 U.S. beef & veal imports increased 54.1% MOM on a daily average basis from the 23 month low experienced in Jan ’16 but remained lower on a YOY basis, finishing down 3.2%. Beef & veal import volumes have declined on a YOY basis for four consecutive months through January. Jan ’16 net beef & veal trade declined to a four month low as the MOM increase in beef & veal imports more than offset the MOM increase in export volumes.

Beef & Veal – Net Trade Declines to Four Month Low on Strong Imports

Jan ’16 U.S. beef & veal export volumes declined 10.9% MOM on a daily average basis but increased on a YOY basis for the first time in 16 months, finishing 7.4% above the previous year’s levels. Of the major export destinations, YOY increases in export volumes were led by South Korea (+51.7%), followed by Japan (+18.4%) and combined volumes to Hong Kong, Taiwan and China (+17.5%). The YOY gains in shipments to South Korea, Japan and China more than offset declines in U.S. beef & veal exports to Mexico (-27.0%) and Canada (-8.0%). U.S. beef & veal exports to the aforementioned countries accounted for over 85% of all beef & veal export volumes during Jan ’16.

Jan ’16 U.S. beef & veal imports increased 54.1% MOM on a daily average basis from the 23 month low experienced in Jan ’16 but remained lower on a YOY basis, finishing down 3.2%. Beef & veal import volumes have declined on a YOY basis for four consecutive months through January. Jan ’16 net beef & veal trade declined to a four month low as the MOM increase in beef & veal imports more than offset the MOM increase in export volumes.

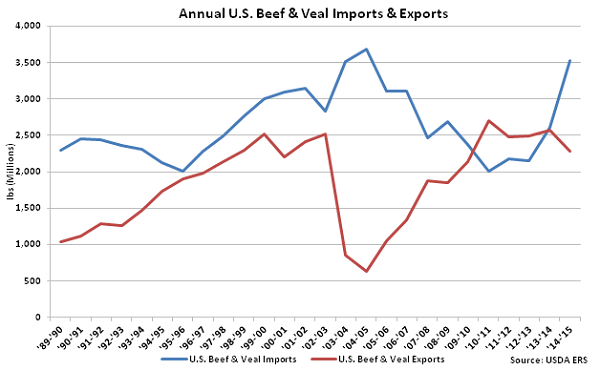

’13-’14 annual U.S. beef & veal imports finished higher than annual U.S. beef & veal exports for the first time in four years. This trend continued into the ’14-’15 production season as annual imports increased to a ten year high and beef & veal net trade declined to an eight year low.

’13-’14 annual U.S. beef & veal imports finished higher than annual U.S. beef & veal exports for the first time in four years. This trend continued into the ’14-’15 production season as annual imports increased to a ten year high and beef & veal net trade declined to an eight year low.

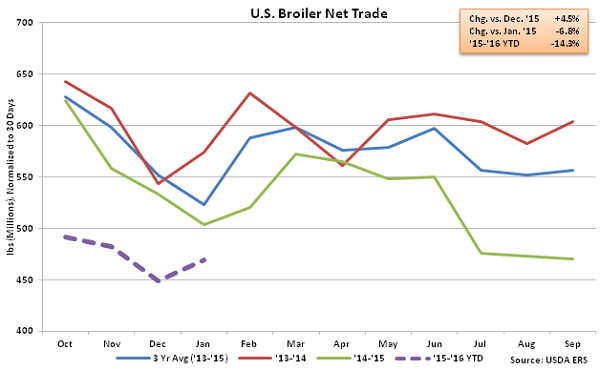

Chicken –Net Trade Declines to a Five Year Low for the Month of January

Jan ’16 U.S. broiler export volumes increased 3.8% MOM on a daily average basis from the four and a half year low experienced in Dec ’15 but remained lower on a YOY basis, finishing 6.2% below the previous year. Monthly export volumes have declined YOY throughout 15 of the past 16 months as demand from several major U.S. broiler import markets remain weak. Combined broiler export volumes to Hong Kong, Taiwan and China increased 6.6% YOY while broiler export volumes to Canada increased 9.8% YOY however the gains were more than offset by an 8.0% YOY decrease in shipments destined to Mexico. Broiler export volumes to Mexico have accounted for nearly a quarter of the total broiler export volumes during Jan ’16.

Jan ’16 U.S. broiler imports continued to increase on a YOY basis, finishing up 25.7%. Broiler imports remain at insignificant levels relative to export volumes, with Jan ’16 imports amounting to only 2.1% of export volumes. Declining broiler exports, coupled with increasing imports, resulted in Jan ’16 net broiler trade declining YOY for the 15th time in the past 16 months, finishing down 6.8% to a five year low for the month of January. Net broiler trade declined 10.9% throughout the ’14-’15 production season and is down an additional 14.3% throughout the first third of the ’15-’16 production season.

Chicken –Net Trade Declines to a Five Year Low for the Month of January

Jan ’16 U.S. broiler export volumes increased 3.8% MOM on a daily average basis from the four and a half year low experienced in Dec ’15 but remained lower on a YOY basis, finishing 6.2% below the previous year. Monthly export volumes have declined YOY throughout 15 of the past 16 months as demand from several major U.S. broiler import markets remain weak. Combined broiler export volumes to Hong Kong, Taiwan and China increased 6.6% YOY while broiler export volumes to Canada increased 9.8% YOY however the gains were more than offset by an 8.0% YOY decrease in shipments destined to Mexico. Broiler export volumes to Mexico have accounted for nearly a quarter of the total broiler export volumes during Jan ’16.

Jan ’16 U.S. broiler imports continued to increase on a YOY basis, finishing up 25.7%. Broiler imports remain at insignificant levels relative to export volumes, with Jan ’16 imports amounting to only 2.1% of export volumes. Declining broiler exports, coupled with increasing imports, resulted in Jan ’16 net broiler trade declining YOY for the 15th time in the past 16 months, finishing down 6.8% to a five year low for the month of January. Net broiler trade declined 10.9% throughout the ’14-’15 production season and is down an additional 14.3% throughout the first third of the ’15-’16 production season.

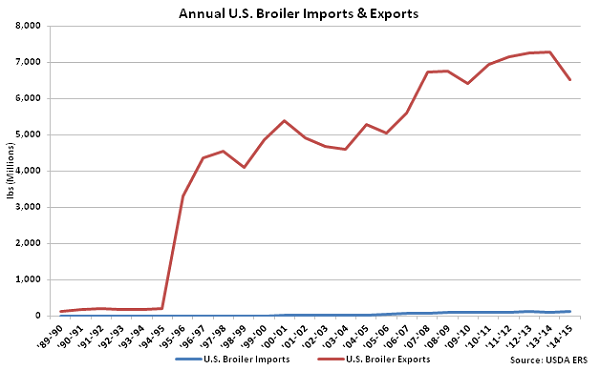

U.S. broiler export volumes have strengthened considerably over the past 25 years, increasing at a compound annual growth rate (CAGR) of 18.3%. U.S. broiler import volumes have increased at a CAGR of 21.6% over the same time period but remain significantly lower. ’13-’14 annual broiler exports volumes were over 60 times as large as import volumes. Broiler export volumes remained 54 times as large as import volumes throughout the ’14-’15 production season despite declining to a five year low on an absolute basis.

U.S. broiler export volumes have strengthened considerably over the past 25 years, increasing at a compound annual growth rate (CAGR) of 18.3%. U.S. broiler import volumes have increased at a CAGR of 21.6% over the same time period but remain significantly lower. ’13-’14 annual broiler exports volumes were over 60 times as large as import volumes. Broiler export volumes remained 54 times as large as import volumes throughout the ’14-’15 production season despite declining to a five year low on an absolute basis.

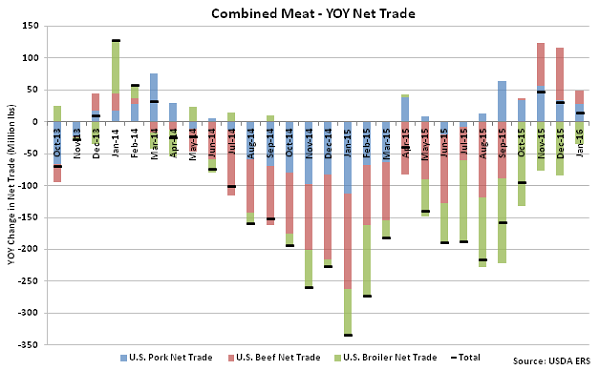

Combined net trade of U.S. pork, beef and broilers increased YOY for the third consecutive month during Jan ’16 as increases in the net trade of pork and beef more than offset a decline in broiler net trade. Combined net trade of pork, beef and broilers had declined for 19 consecutive months from Apr ’14 – Oct ’15 and finished down 21.4% YOY throughout the ’14-’15 production season.

Combined net trade of U.S. pork, beef and broilers increased YOY for the third consecutive month during Jan ’16 as increases in the net trade of pork and beef more than offset a decline in broiler net trade. Combined net trade of pork, beef and broilers had declined for 19 consecutive months from Apr ’14 – Oct ’15 and finished down 21.4% YOY throughout the ’14-’15 production season.

U.S. pork export volumes have strengthened considerably over the past 25 years, increasing at a compound annual growth rate (CAGR) of 13.2%, while U.S. pork imports have remained fairly flat, increasing at a CAGR of 0.3% over the same time period. ’13-’14 annual pork imports experienced much stronger growth, finishing 10.5% higher than the previous year, the largest YOY percentage gain in 11 years. Despite the increase in pork imports, ’13-’14 annual pork exports volumes remained over five times as large as import volumes. Pork export volumes remained over four times as large as import volumes throughout the ’14-’15 production season despite declining to a five year low on an absolute basis.

Beef & Veal – Net Trade Declines to Four Month Low on Strong Imports

Jan ’16 U.S. beef & veal export volumes declined 10.9% MOM on a daily average basis but increased on a YOY basis for the first time in 16 months, finishing 7.4% above the previous year’s levels. Of the major export destinations, YOY increases in export volumes were led by South Korea (+51.7%), followed by Japan (+18.4%) and combined volumes to Hong Kong, Taiwan and China (+17.5%). The YOY gains in shipments to South Korea, Japan and China more than offset declines in U.S. beef & veal exports to Mexico (-27.0%) and Canada (-8.0%). U.S. beef & veal exports to the aforementioned countries accounted for over 85% of all beef & veal export volumes during Jan ’16.

Jan ’16 U.S. beef & veal imports increased 54.1% MOM on a daily average basis from the 23 month low experienced in Jan ’16 but remained lower on a YOY basis, finishing down 3.2%. Beef & veal import volumes have declined on a YOY basis for four consecutive months through January. Jan ’16 net beef & veal trade declined to a four month low as the MOM increase in beef & veal imports more than offset the MOM increase in export volumes.

’13-’14 annual U.S. beef & veal imports finished higher than annual U.S. beef & veal exports for the first time in four years. This trend continued into the ’14-’15 production season as annual imports increased to a ten year high and beef & veal net trade declined to an eight year low.

Chicken –Net Trade Declines to a Five Year Low for the Month of January

Jan ’16 U.S. broiler export volumes increased 3.8% MOM on a daily average basis from the four and a half year low experienced in Dec ’15 but remained lower on a YOY basis, finishing 6.2% below the previous year. Monthly export volumes have declined YOY throughout 15 of the past 16 months as demand from several major U.S. broiler import markets remain weak. Combined broiler export volumes to Hong Kong, Taiwan and China increased 6.6% YOY while broiler export volumes to Canada increased 9.8% YOY however the gains were more than offset by an 8.0% YOY decrease in shipments destined to Mexico. Broiler export volumes to Mexico have accounted for nearly a quarter of the total broiler export volumes during Jan ’16.

Jan ’16 U.S. broiler imports continued to increase on a YOY basis, finishing up 25.7%. Broiler imports remain at insignificant levels relative to export volumes, with Jan ’16 imports amounting to only 2.1% of export volumes. Declining broiler exports, coupled with increasing imports, resulted in Jan ’16 net broiler trade declining YOY for the 15th time in the past 16 months, finishing down 6.8% to a five year low for the month of January. Net broiler trade declined 10.9% throughout the ’14-’15 production season and is down an additional 14.3% throughout the first third of the ’15-’16 production season.

U.S. broiler export volumes have strengthened considerably over the past 25 years, increasing at a compound annual growth rate (CAGR) of 18.3%. U.S. broiler import volumes have increased at a CAGR of 21.6% over the same time period but remain significantly lower. ’13-’14 annual broiler exports volumes were over 60 times as large as import volumes. Broiler export volumes remained 54 times as large as import volumes throughout the ’14-’15 production season despite declining to a five year low on an absolute basis.

Combined net trade of U.S. pork, beef and broilers increased YOY for the third consecutive month during Jan ’16 as increases in the net trade of pork and beef more than offset a decline in broiler net trade. Combined net trade of pork, beef and broilers had declined for 19 consecutive months from Apr ’14 – Oct ’15 and finished down 21.4% YOY throughout the ’14-’15 production season.